Concentrated Capital - Shutdown and Macro Update

Bear market is now consensus. Double sell off on crypto cycle exhaustion and AI bubble fears. Fresh set of venture deals.

I usually aim to deliver Concentrated Weekly to your inbox Friday morning, publishing this week off schedule and lighter touch than usual due to Devconnect Argentina. Ethereum conferences start to remind me of Linux and Android ecosystems: core values, cypherpunk, hard engineering problems, balanced with less polished production quality and ecosystem fragmentation.

Macro - All eyes on Fed and TGA

S&P started its correction when, on Oct 29, the Fed expectedly cut rates by 25 bps but mentioned that the December rate cut is far from given, which triggered markets repricing cuts. Before these remarks, the market was pricing in steady 25 bps decreases toward the long-term target of 2.75%.

Last week Thursday’s sell off deepened on the Fed telegraphing no rate cut in December by multiple channels (FED’S DALY: REALLY THINK THERE IS A PREMIUM ON WAITING TO DECIDE ON RATES UNTIL YOU HAVE AS MUCH INFORMATION — https://x.com/BloombergTV/status/1988981949826757013?s=20). Chances of a rate cut were lowered to 40% on Polymarket.

Government reopen on Nov 12 provided a small relief rally, an opportunity to go further risk off (I have not used that).

AI bubble fears still going through the market with Oracle CDS uptick. Nvidia highly beating expectations on earnings has not helped the market recover, erasing gains the same day as analysts are concerned with Nvidia financing its clients. Example: $10B Anthropic deal leading to $30B in promised datacenter usage — https://www.bloomberg.com/news/articles/2025-11-20/a-hedge-against-ai-crash-emerges-as-oracle-cds-market-explodes.

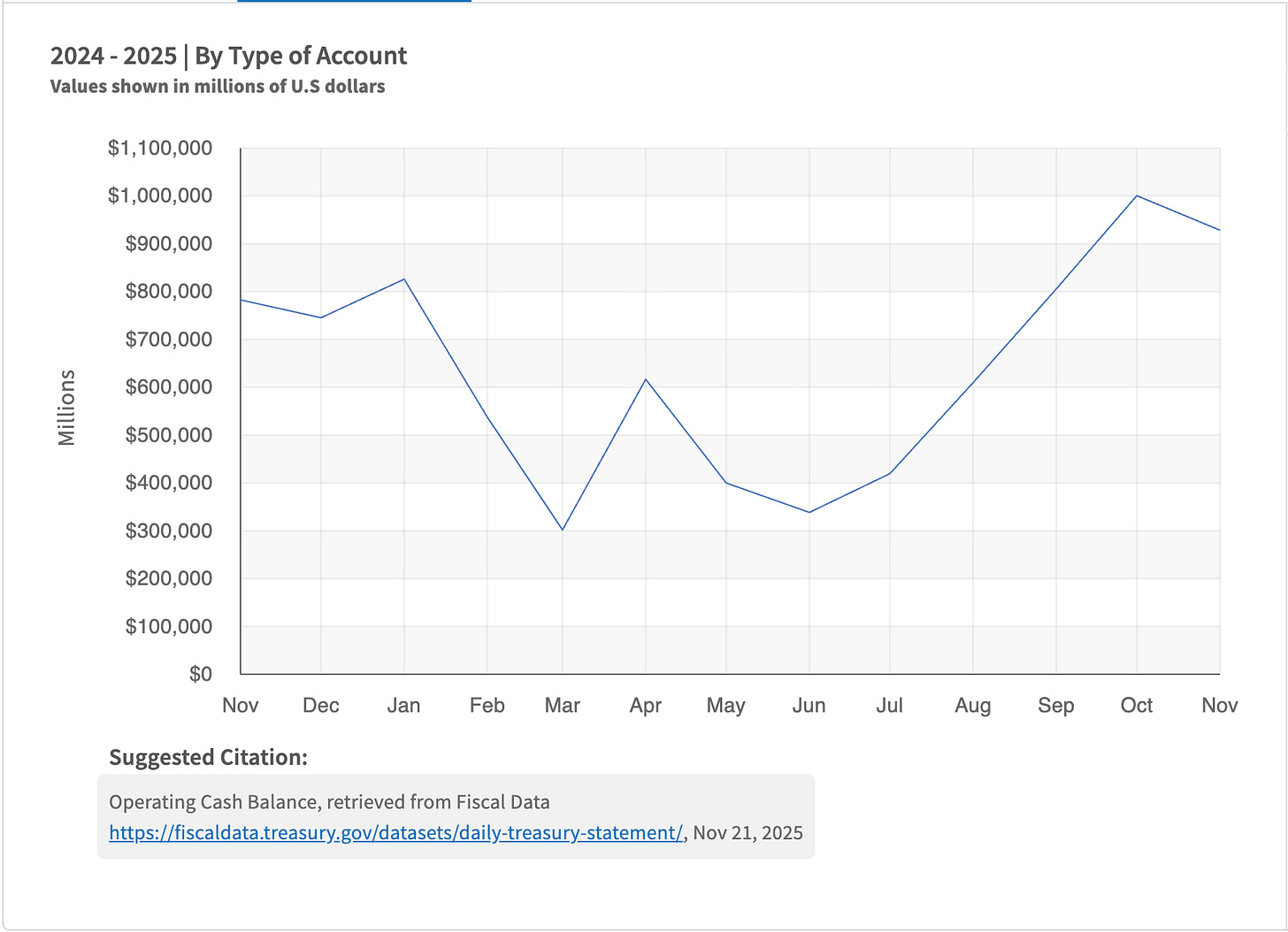

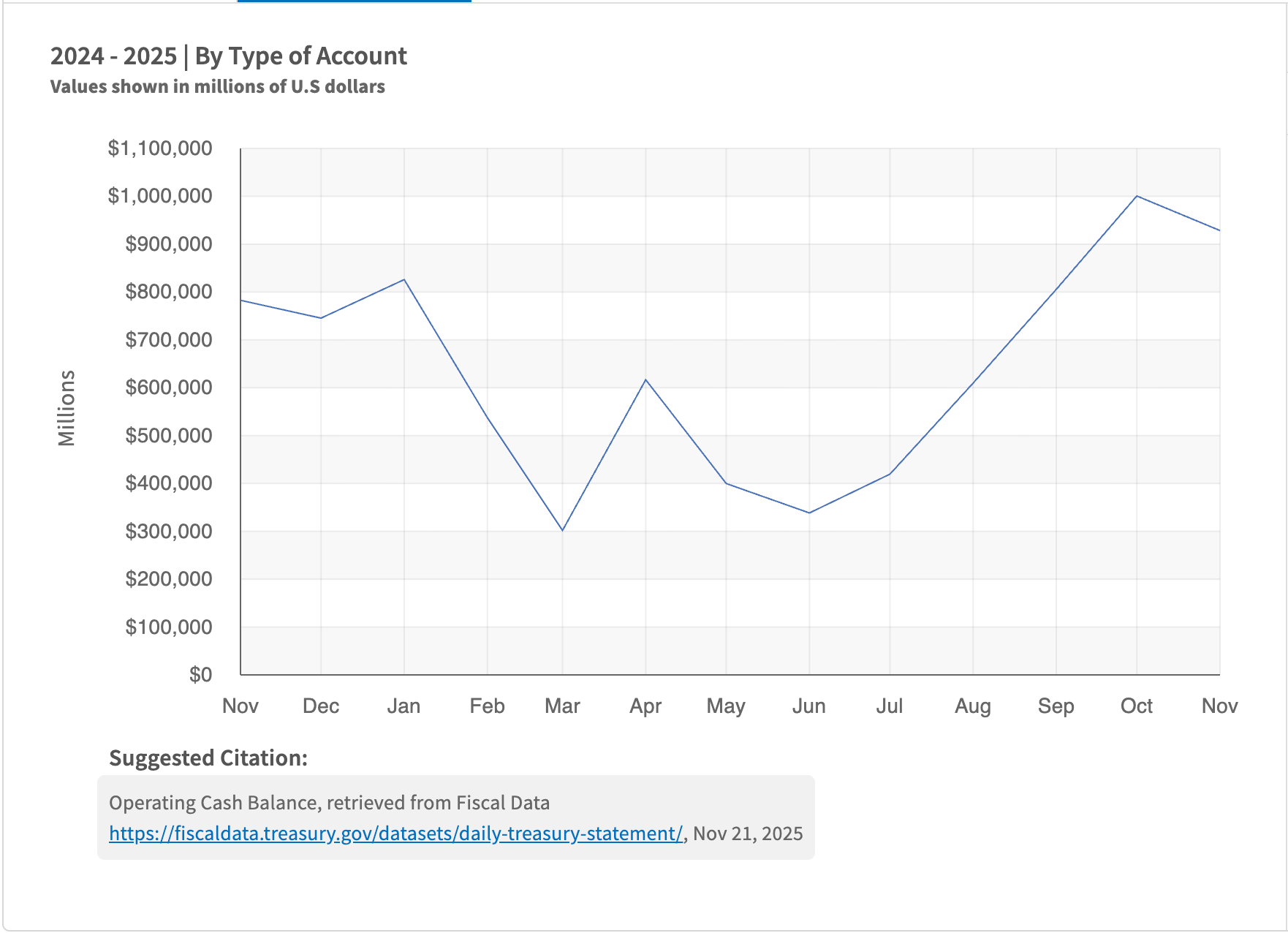

Macro is healing: TGA has just started to be spent down from $1T to $928B as of Nov 19. Meaningful spend of $200–300B and a couple weeks’ delay is positioning us for the end of macro correction in December — https://x.com/zerohedge/status/1990765251810505143 and https://fiscaldata.treasury.gov/datasets/daily-treasury-statement/operating-cash-balance

.

While first cracks appear in the AI theme, it’s far from doom and gloom. I do not expect a proper bubble bust right now up until the OpenAI IPO. When OpenAI starts to publish quarterly revenue, it’s going to be more obvious that revenue growth is slower than expected by all this spending. Convergence of bear market crypto and AI bubble burst will create a great buying opportunity at the end of 2026 to first half of 2027.

Industry Notes:

What’s driving the crypto bear market aside from macro weakness? Santiago from Inversion Capital published a newsletter and a podcast with a simple headline: Have we earned being a $3T industry? We’ve got everything we wanted from regulatory support, institutional adoption, and ETF flows, yet still struggled to attract users with wallet counts sitting at 30–60m monthly active. Ethereum is trading at 200–400x P/S (not P/E), and Solana is trading at 20–60x P/S (far more reasonable btw). https://x.com/santiagoroel/status/1990430092997050753 and https://x.com/santiagoroel/status/1991877125516009513.

Monad ICO has shown weakness, being filled only 35% after a couple of days. Currently we’re sitting at a 90% fill ratio one day before the sale end. This reminds me of 2017 ICO days, when ICOs were bid first two days and last two days. Struggling to fill but filling eventually shows correct pricing — not leaving money on the table, while still showing overall market weakness.

Circle is back below its first day trading open at $69. The highest performing IPO of the year gave it all back, but still is way above the IPO price of $31. Circle has an incredible network effect which it will find a way to monetize and is a great candidate for a 2026–27 buying spree.

Deals

Introducing a new category in Weekly with updates regarding the deals I’ve entered before or am considering now. I’m going to be publishing interesting targets even if I’m not bidding due to off-thesis or other reasons, so feel free to reach out for an intro.

Kraken - tiny bright spot of hope amid the bloodbath - has announced a $200m round at $20B from Citadel as well as confidentially filing for IPO in Q1 2026. Latest earnings show Q3 $628m revenue (+50% QoQ, +112% YoY) and $178m adjusted EBITDA (+124% QoQ). https://blog.kraken.com/news/q3-2025-financial-highlights. I entered this deal at $10B. Kraken is one of the few companies that can still pull off an IPO in this market, but I don’t expect them to repeat Circle success, targeting a conservative $25–30B valuation.

XPlace - pre seed Solana credit card company, a competitor of Pyra. Similar to Etherfi Cash model, where you can spend from the card borrowing against your SOL holdings. Founded by a UK team with prior experience in microcredits for the Mexico market. Excited about this one, though card issuing crypto neobanks are oversaturated, and I’m still lacking this fintech DD framework, which I’m working on.

Early stage Hyperliquid mobile trading app by Suhil Kakar from TAC. Unbranded yet. Hyperliquid native app is generally the market category I’m excited about.

Brightside.gg by Yash Jhade - lighter mobile trading app similar to the above, notably not as crowded as Hyperliquid, while Lighter is steady #3 by perp DEX open interest behind Hype and Aster.

Partner VC deals: Embed Protocol - token/action recommendation model for onchain users with Coinbase and Farcaster as clients. Overherd - anonymous social network with USDC payouts by Yik Yak founder. Blockscout - veteran crypto blockchain explorer by Igor Barinov.