Concentrated Research: Circle Hyperscaler Memo

Crypto has it’s own set of hyperscalers that just get bigger and better all the time

Mood and bias of the memo

Imagine a world where ALL CRYPTO is gone — or, even better, never existed — except for USDC and USDT. I still see it as a massive success and implementation of half of the original Bitcoin thesis. And I still see it 10× from here.

Cycle Awareness

As mentioned in our https://blog.concentrated.vc/p/concentrated-capital-four-year-cycle I’m a strong believer in the inherent decaying four-year cycle, so I’m looking at Circle data through the cycle lens. I believe both Circle fundamentals and price are correlated to the cycle.

Nature of stablecoin business

This is a critical part that many of the people have inside out (they have it backwards). It’s often considered that the nature of the stablecoin business is revolving around value storage and a corresponding yield. Usually the believers of this core offering believe in the inevitable fracturing of the stablecoin landscape and Circle’s market share being decimated.

As a founder running a network effect business and battling against a network effect business I know when I see one. While the worldwide desire to store value in United States Dollars exist and is a strong one, everyone who’s storing the value is highly considered ****about security of that storage, and in any form of money case security relies on trust and acceptance of that currency.

Both Tether and Circle are not so universally redeemable as they seem to be - they are redeemed by approved entities: Minters. So for everyone outside the minters’ circle, redeemability comes down to who are the parties accepting this coin as a payment or ready to exchange it for other valuables.

On top of that comes the second stablecoin use after storage - value transfer. Arguably this is an even more important stablecoin use case than storage, as we’re evidently seeing people who have access to other forms of storage using stablecoins purely for transaction purposes. This part is even more obviously dependent on the network of who you can transfer to.

Thus: the nature of the stablecoin business is its network of acceptance

Earning yield on reserve and passing it on it’s users or not is ultimately a secondary component - monetization of the network. Useful thought experiment would be - trying to imagine we live in a world of 0 rates, do people still use Tether and Circle?

Fundamentals

Fundamentals are best when looking at the business as it is: the network.

What does the entire network look like, what’s its size and growth?

Who are the key nodes/hubs of the network?

What sub-networks exist and what are their market shares?

So, let’s look together.

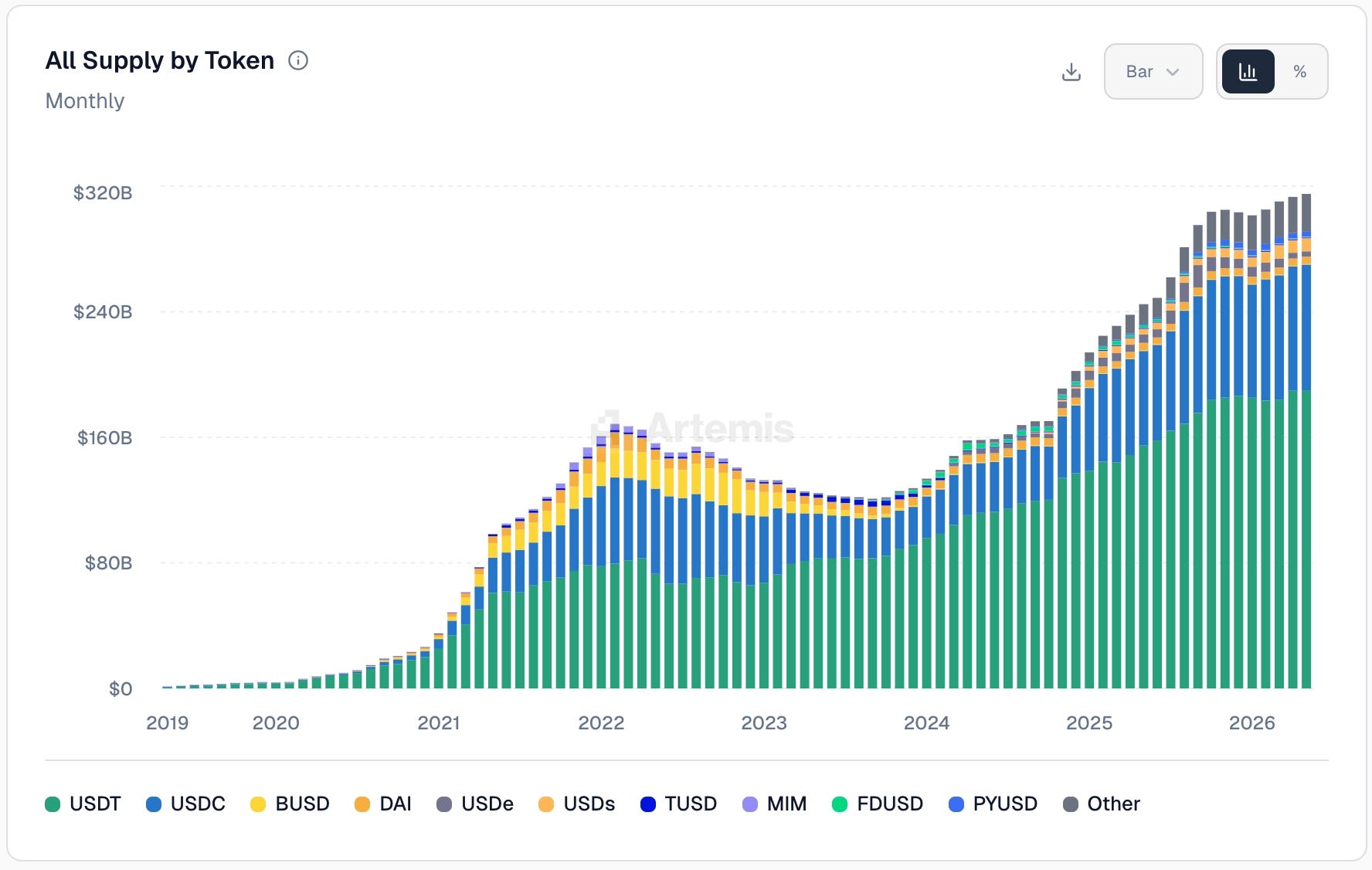

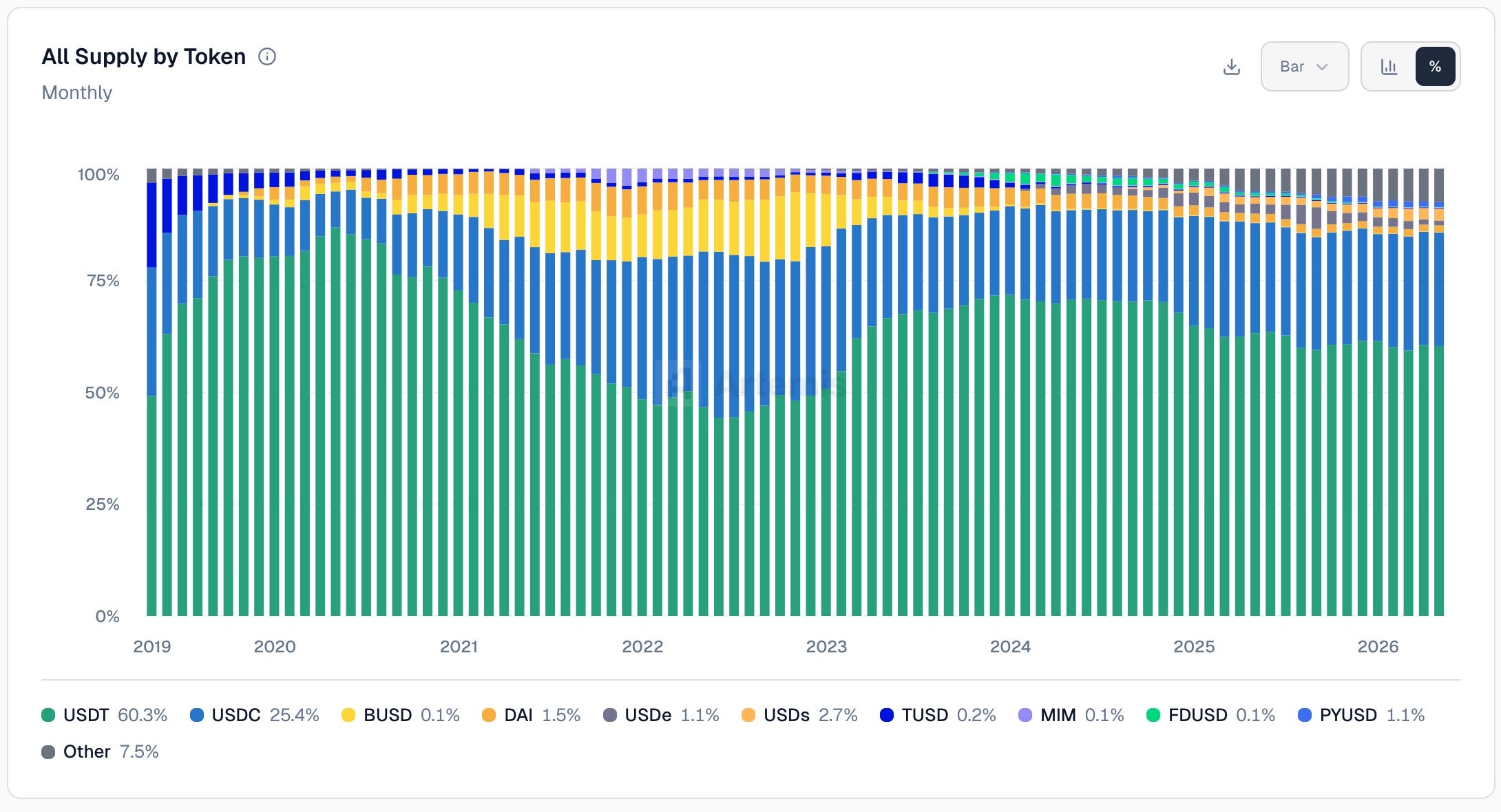

Entire stablecoins network

While not entirely representative, the most accurate metric available is Stablecoin supply. We’re sitting at around $315B total stablecoin supply — all-time high despite the downcycle.

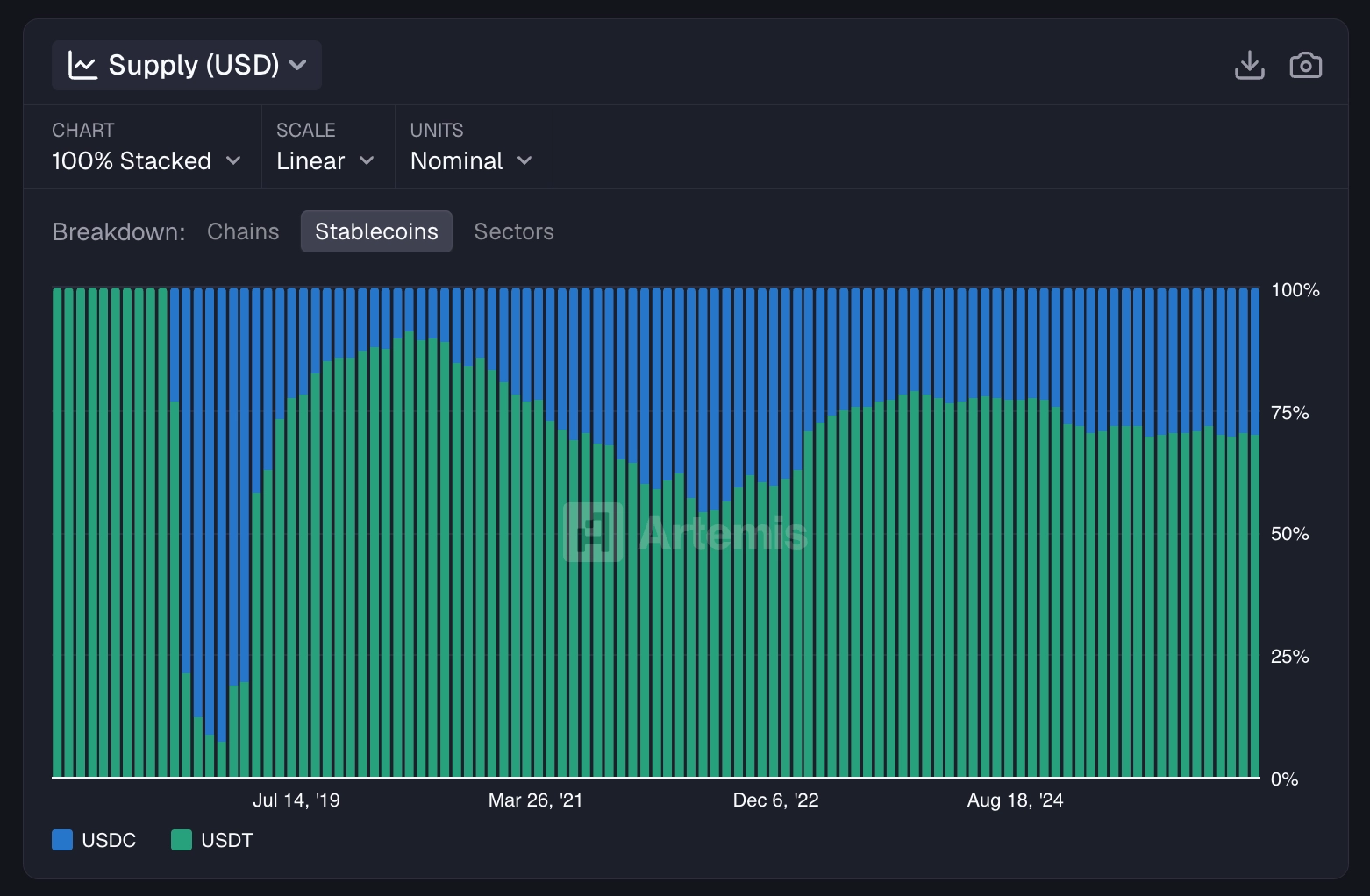

Two obvious players are dominating the market, let’s explore the network structure for both of them: Tether 60%, Circle 25% of the market.

Tether

The oldest stablecoin, the leader, the offshore eurodollar.

Key network players:

Asian exchanges

Crypto OTC brokers worldwide

Retail offshore users worldwide

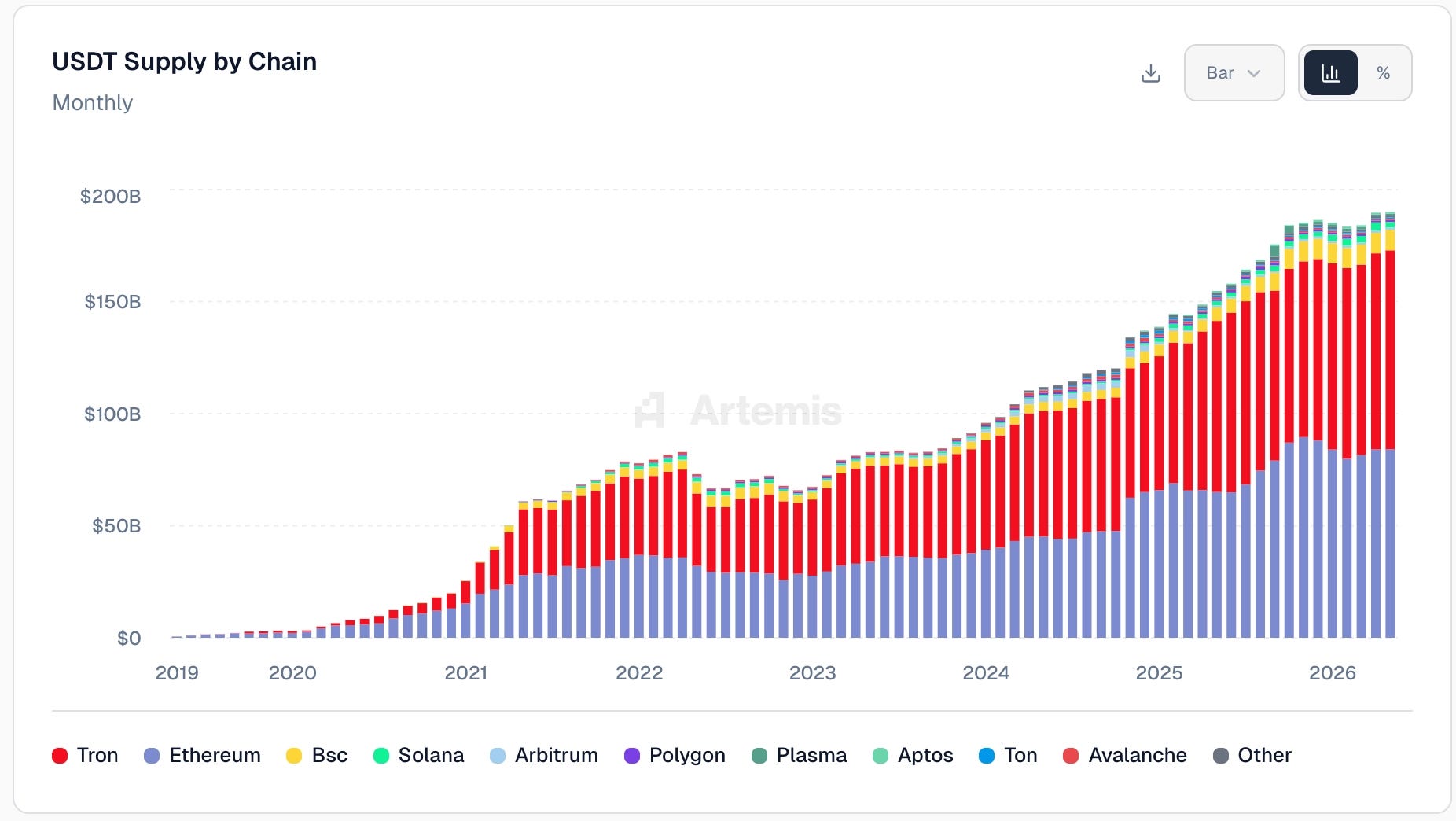

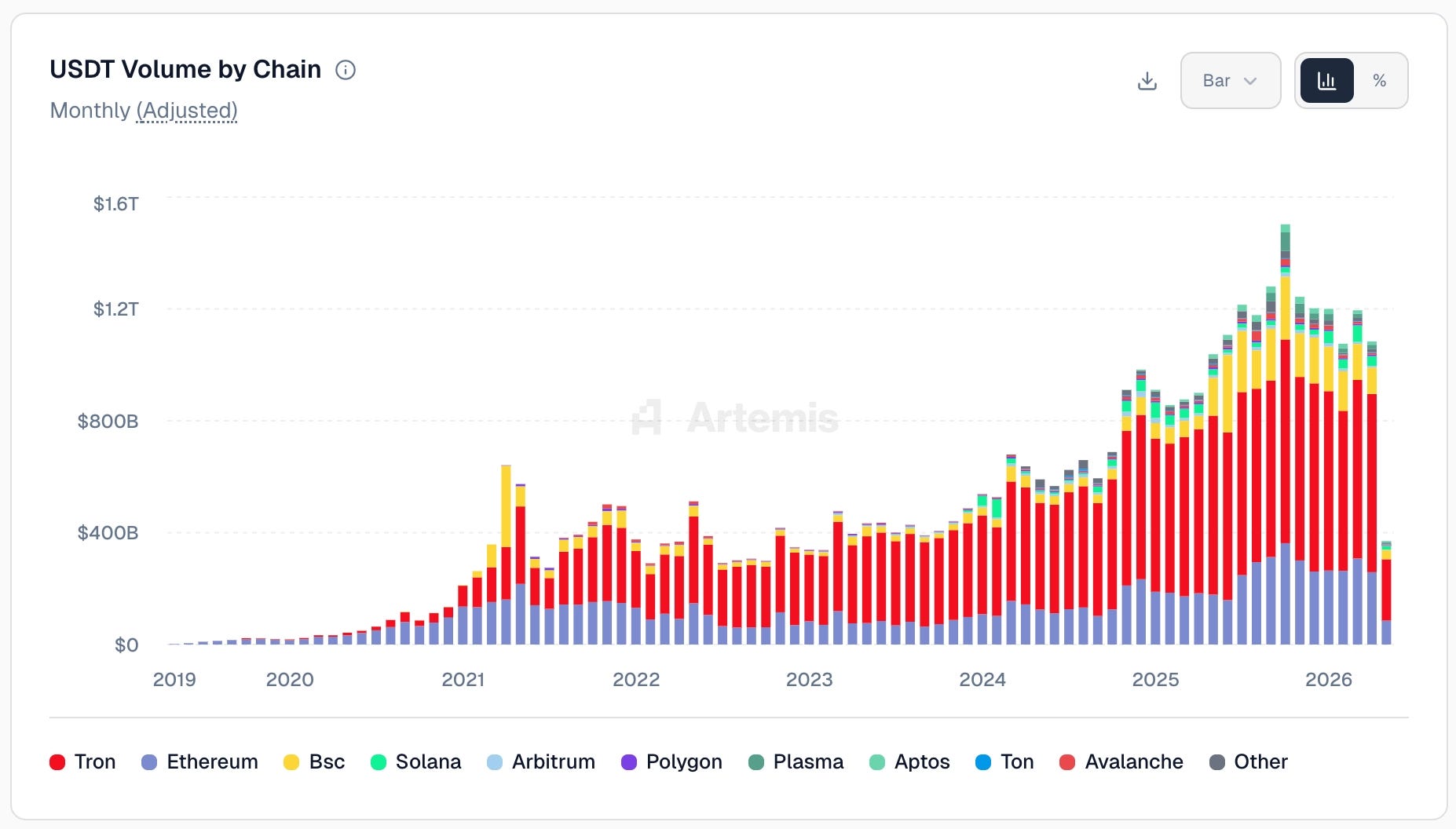

$190B Total supply with 46% on Tron

$1.1T monthly adjusted volume with 56% of volume on Tron and 8.5% on BSC

Circle

“The compliant one”

Key network players:

US and European Exchanges

Onchain DeFi

New: Banks and financial institutions!

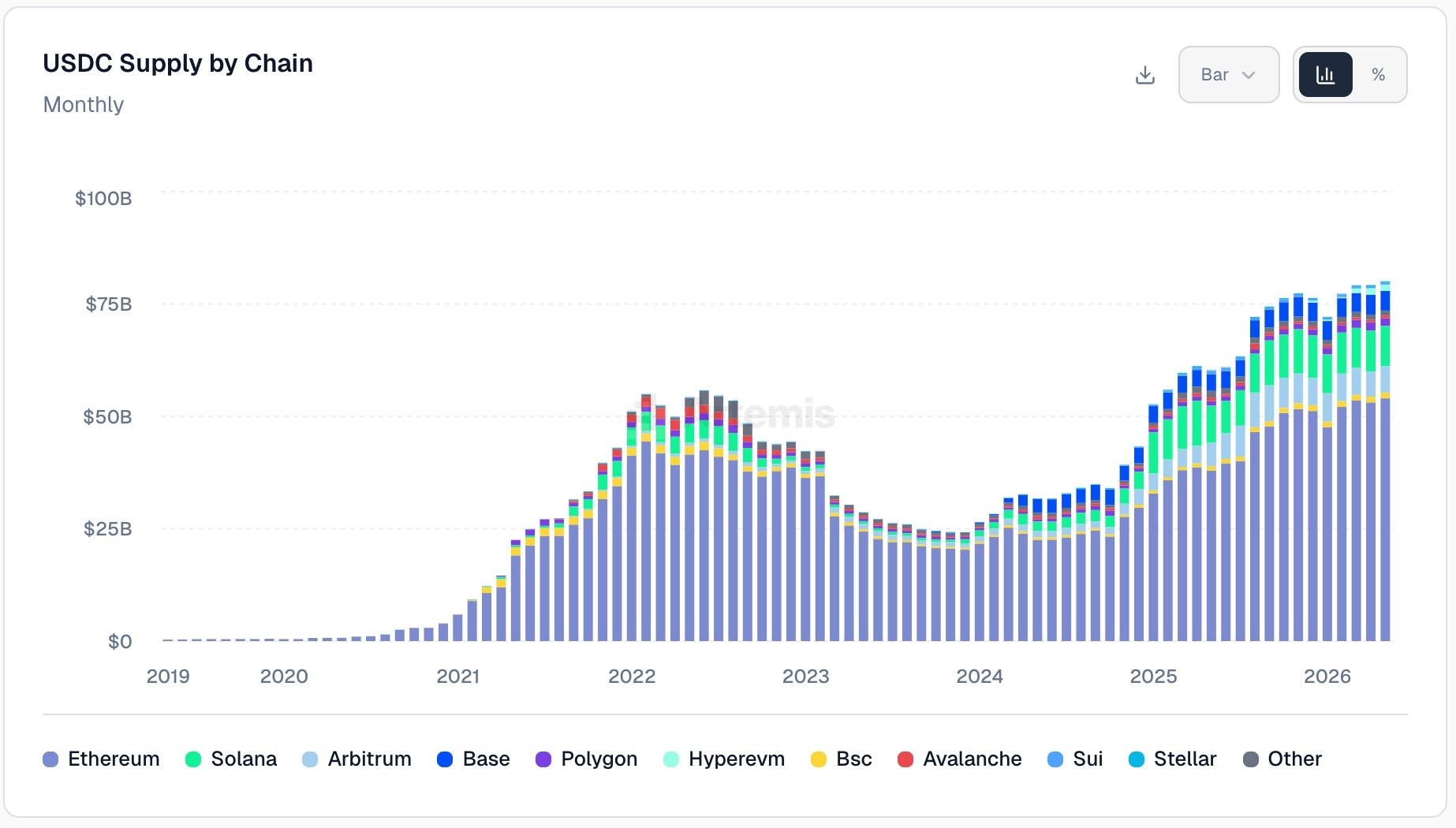

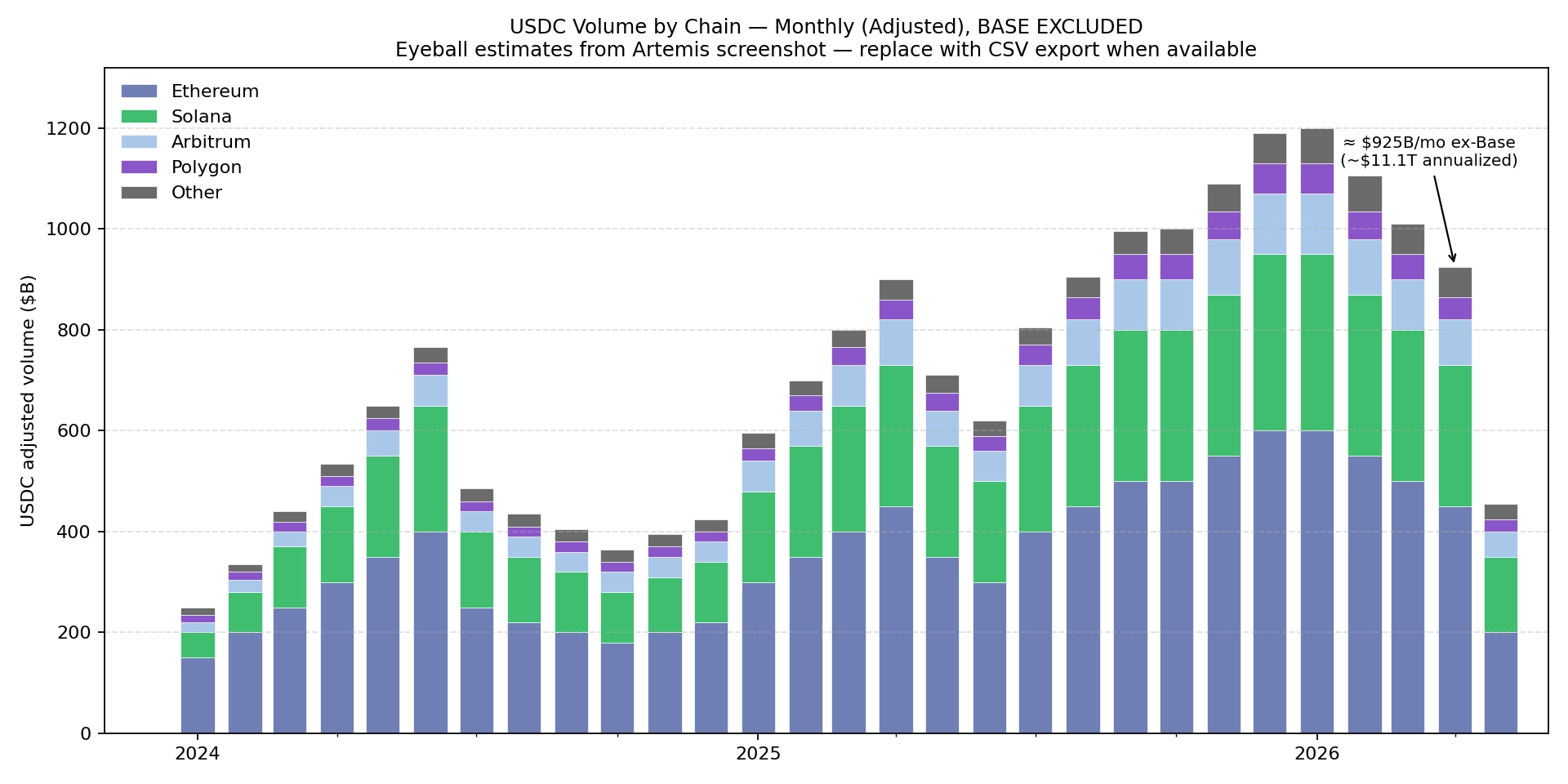

$80B - Total Supply with 67% on Ethereum

~$900B - Monthly adjusted volume

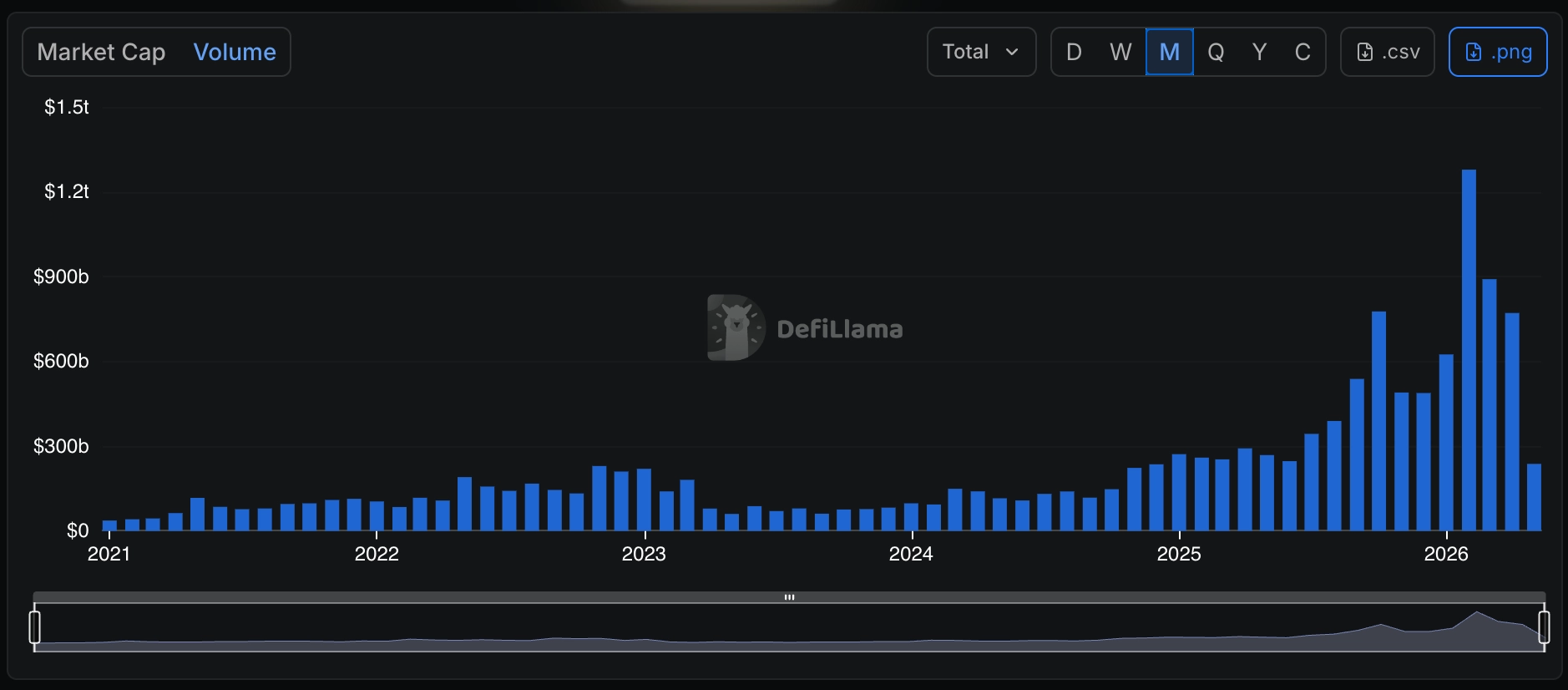

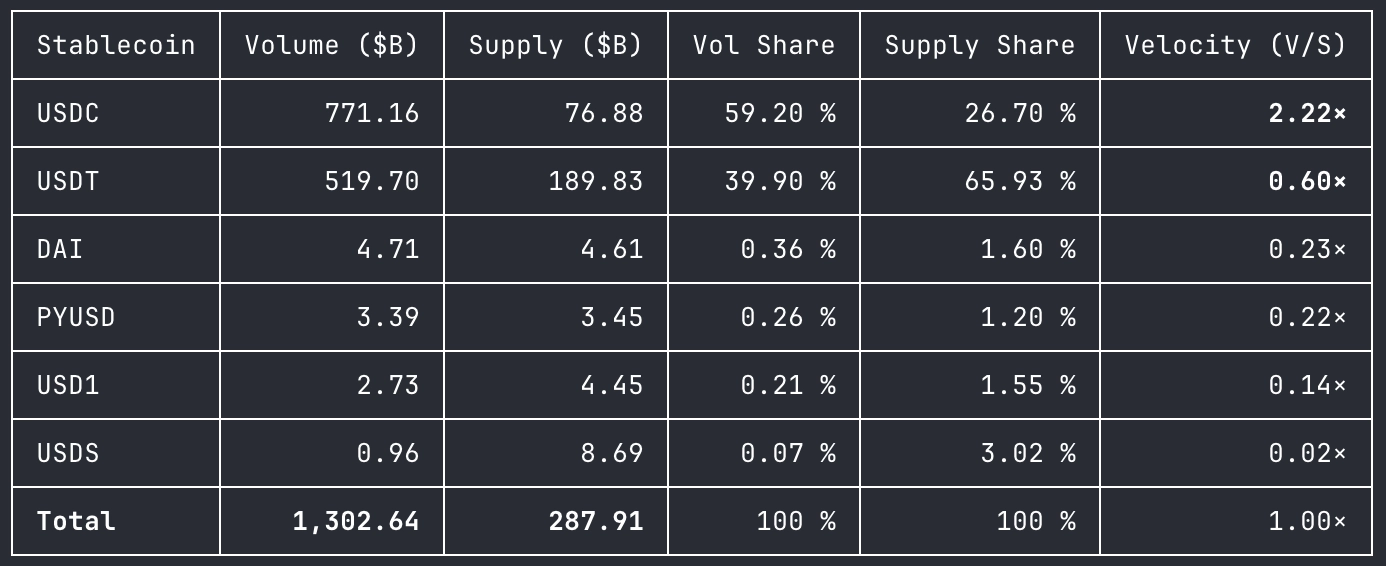

Transaction volume

DeFiLlama and Artemis report similar $900B adjusted volume. (Given we exclude Base from Artemis Data)

Bottom line:

Circle and Tether are a lot more alike than different. Classic duopoly — Tether holds the bigger offshore network, Circle is onshore, smaller but has higher velocity of money.

Network is highly partitioned. Different chains, geographies, network participants

Market shares are stable. No drift towards USDT, last meaningful change was during SVB collapse

Non-payment-network stablecoins are tokenized deposits

From the outside it might look like the duopoly is vulnerable, as several competitive stablecoins managed to amass meaningful supply in billions of dollars.

The biggest being Sky ecosystem of USDS and DAI of $13B or 4.6% supply market share.

Ethena managed to be of similar size last cycle,

PYUSD is a compliant contestant from a non-crypto native payment network

At a closer look all of them failed to attract meaningful network effects and payment use-cases.

We might see a lot of these branded stablecoins coming, but all of them are ultimately going to resemble tokenized deposits — parking money with a specific institution and not expecting any interoperability.

Bear case and risks for the network

Below we’re going to try to map out realistic risk scenarios from a network effect vantage point:

1 — Winner takes it all: USDT consumes the entire network

The classic risk in a network effect business - the biggest network grows from 60% market share to 90% market share. In an open network without strong partitioning it happens all the time. One of the best examples is Uniswap on ETH L1 — it was extremely hard to compete against it, and Balancer, Curve and everyone else have died because of network effects. Hyperliquid is showing similar traction.

The clear example of partitioning is CEXs: geography and regulation created explicit walls in the network architecture. Coinbase is inherently separated from Binance, and this is what allows the meaningful market share stability.

We argue that similar mechanics with strong partitioning exist between USDC and USDT — the GENIUS Act has exacerbated that partitioning by rendering USDT non-compliant with it.

USAT has to build network effects from scratch, which is going to be hard. Still, Tether’s war chest and relationship base make it enough of a risk to be listed here.

2 — A new competitive network from a consortium of US Banks

Circle was created as a consortium, and the only credible way to new network creation would follow a similar path. If top 10 banks in US join forces and create a compliant shared stablecoin that’s accepted as a means to transact between these banks it can create a meaningful network effect off the bat, possibly sized enough to rival Circle right away.

What increases the risk is that the banks announced this exact initiative a year ago https://www.coindesk.com/business/2025/05/23/major-us-banks-mull-jointly-launching-stablecoin-wsj

We maintain an opinion that needed level of coordination makes it an uphill battle and the banks are going to focus on issuing their own stablecoins-turning-tokenized-deposits. https://blockeden.xyz/blog/2026/03/14/wells-fargo-wfusd-stablecoin-fourth-largest-us-bank-enters-race/

3 — Tokenized deposits develop collective interoperability

That’s a longer term risk resembling the path of establishing the US bank system itself: individual disjointed deposits were unified and started to be cross accepted between each other ultimately giving birth to a common denominated dollar system. With the interoperability onchain this is a possible scenario.

While being theoretically strong, the time horizon places it outside the near-term (5-year) window.

Bull case for the network

Bull case for the network - growth of the compliant part of the network faster than offshore one without any meaningful competition. Core new groups of network nodes:

Crypto-native hyperscalers outside of Coinbase

Hyperliquid - holds $5B of USDC supply today.

Polymarket - $500M of USDC

Lighter - $500M of USDC

Financial institutions

Latest cohort of institutions adding support for USDC includes:

Erebor

Slash

Interactive Brokers

Meta

Doordash

Stripe

Visa

Shopify

Announced in works

Mercury

Brex

So while the consortium of banks is trying to design their own stablecoin, the fresh cohort of neobanks is already supporting USDC — and time is on Circle’s side.

Aside from that, crypto-adjacent institutions are getting promoted in the plumbing system and granted OCC National Trust Bank Charters

Anchorage, Circle, Ripple, Bitgo, Paxos, Bridge, Crypto.com, Coinbase

Pending: Kraken, ZeroHash, WLFI

Financials (Q1 and 2026 projections)

Let’s examine the back of the envelope major financial parameters of a duopoly

1. Reserve Income

Read: Tether reserve composition (74% Treasuries + 26% BTC/gold/secured loans/cash) blends to ~4.5% vs Circle’s ~3.5% pure-Treasury yield - a structural ~100 bps premium that holds through cycle.

Q1 2026 looked soft for Tether ($1.04B reported net profit) because BTC/gold MTM underperformance, the structural 4.5% rate normalizes through the year.

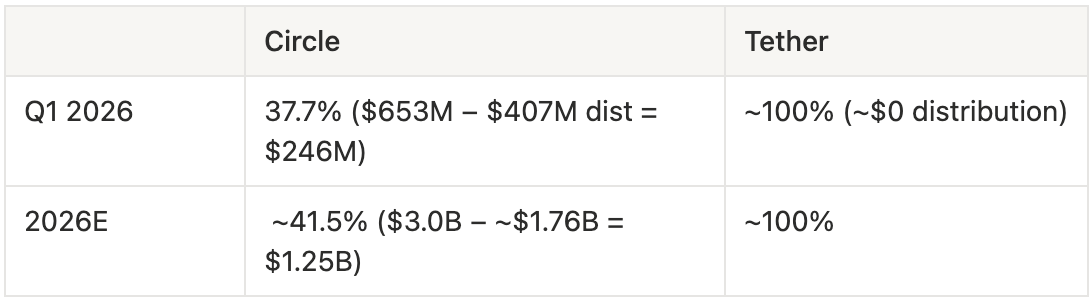

2. Net reserve revenue margin (after distribution)

Read: This is the single biggest fact in the entire Circle thesis. Tether keeps ~$1.00 of every $1.00 of reserve income; Circle keeps $0.42. The 2.4× margin gap is the Coinbase tax. Circle’s margin expands Q1 → 2026E (38% → 42%) on operating leverage as Other Revenue grows faster than distribution costs, but it remains structurally capped well below Tether.

3. Net reserve revenue (after distribution)

Read: Circle’s share collapses from 30% on supply to 12–13% on net reserve dollars.

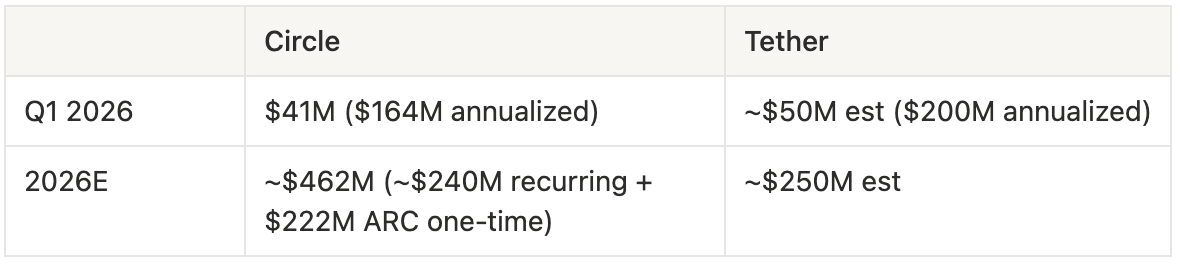

4. Circle wildcard - Non-core net revenue

CPN take-rate (~$10B+ ann. payment volume × take-rate): ~$60–80M

USYC management fee ($3B+ AUM × ~50 bps): ~$15–25M

Subscription / API / Mint services / treasury services: ~$130–150M

Agent Stack — excluded (immaterial; modeled separately as up to $50M by 2029)

ARC token presale (one-time, May 11, 2026): $222M

Read: Recurring non-core is ~$240M for 2026. Around ~20% of total Net Revenue, modest undertaking of Circle to diversify the revenue streams. If we count ARC token revenue alternative revenue streams grow to a meaningful ~37%

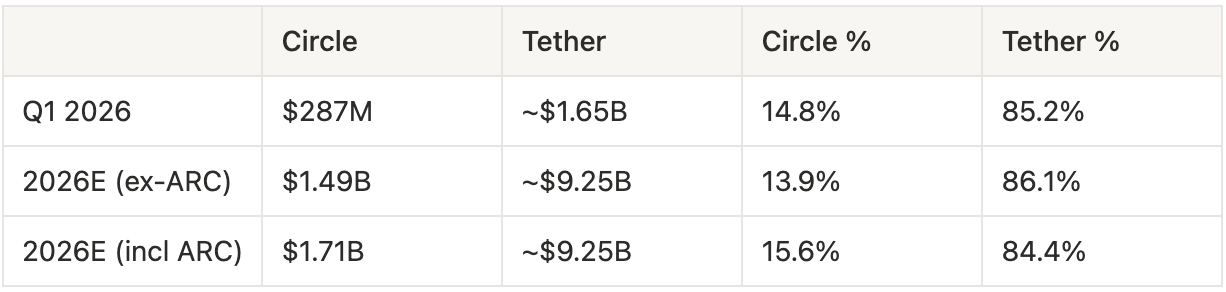

5. Total net revenue

Read: Circle’s share stays in the 14–16% band. The ARC kicker is now the only thing pulling Circle above 14% in 2026E.

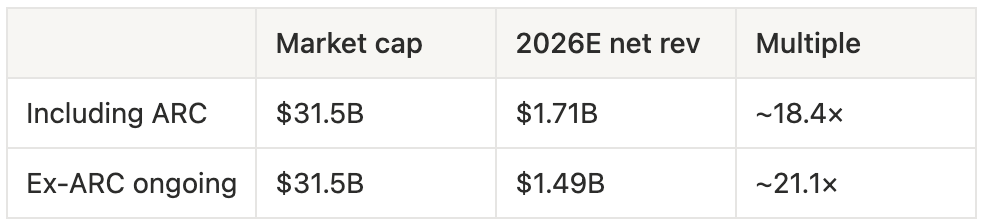

6. Forward net revenue multiples

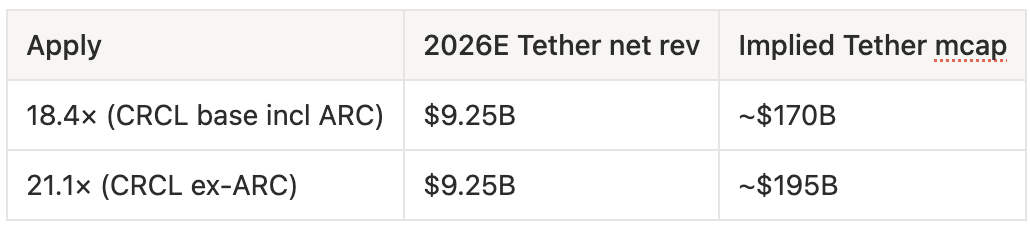

7. Implied Tether valuation at CRCL multiples

vs CRCL at $31.5B mcap today.

Public comparable multiples

Company Forward multiple

Visa ~13×

Mastercard ~14×

Coinbase ~7–8×

PayPal ~2×

Circle ~18–21×

Elephant in the room

Coinbase owns half (or more) of Circle’s economics — why not just get exposure through COIN? Let’s examine that

Indeed Coinbase has a perpetual agreement with Circle that CB keeps

100% of reserve income on USDC held on Coinbase (around 25% of all USDC)

50% of reserve income on all other USDC

In perpetuity unless mutually agreed otherwise

Evaluating the Coinbase’s part of Circle revenue

One key point is that Coinbase doesn’t keep all of the distributions; a significant part of it is passed to the users for holding USDC on Coinbase’s balance. Which in turn works as a shared acquisition cost between USDC itself and CB as a platform.

Q1 2026 Data:

Coinbase Q1 2026 total revenue: $1.4B with stablecoin share:

$305.4M is 21.7%

$192.0M is 13.7% (excluding user pass through revenue)

If we apply a Naive Share of Revenue of Coinbase Market Cap we get:

$51B × 21.7% = $11B

Which means half of Circle’s gross revenue that is passed to Coinbase is valued at almost a 2/3 discount inside Coinbase.

Now, Coinbase has a counterparty risk of renegotiated contract plus no access to residual non USDC revenue of Circle. But the number is still high.

One could argue that Coinbase is indeed the better exposure to Circle

Momentum

If Coinbase gives you almost everything Circle does + the entire Coinbase business for just $20B on top, why buy Circle at all?

Momentum

Retail Narrative

It is hard to put it in numbers but perception is

Stablecoins = CRCL

Crypto = COIN

Last cycle, on the back of the GENIUS Act, Circle was trading at a 74× Net Revenue multiple (31× Gross Revenue multiple)

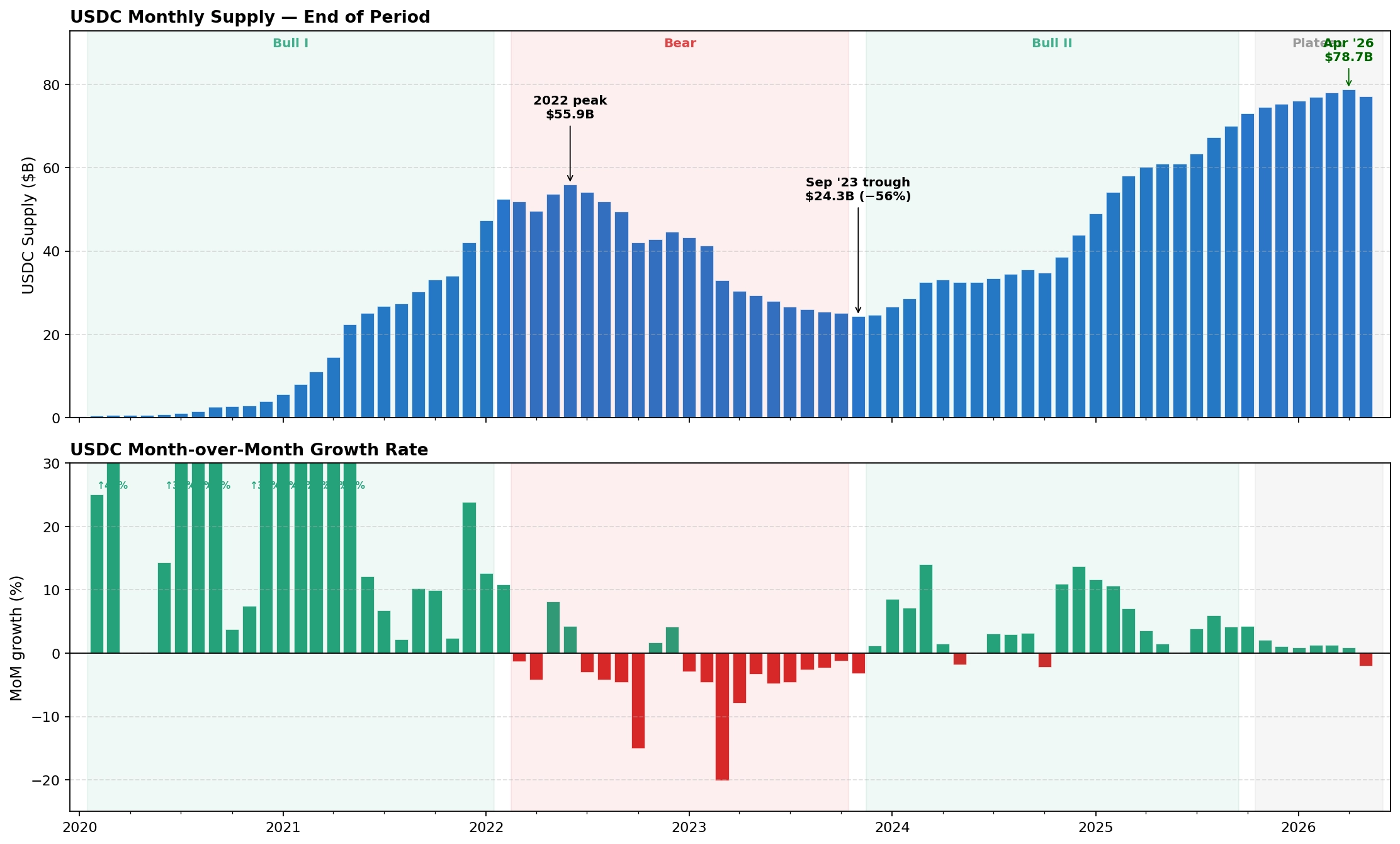

Below is the chart showing the cyclicality of the supply. A lot of the supply reduction was driven by SVB collapse last cycle but not all of it. The fact that there’s almost no supply reduction this cycle is overall bullish.

10% MoM Supply growth at the cycle peak is 300% annualized growth that the market “feels” in the moment. So we might see a return of 40x net revenue multiple at the peak of the bull run

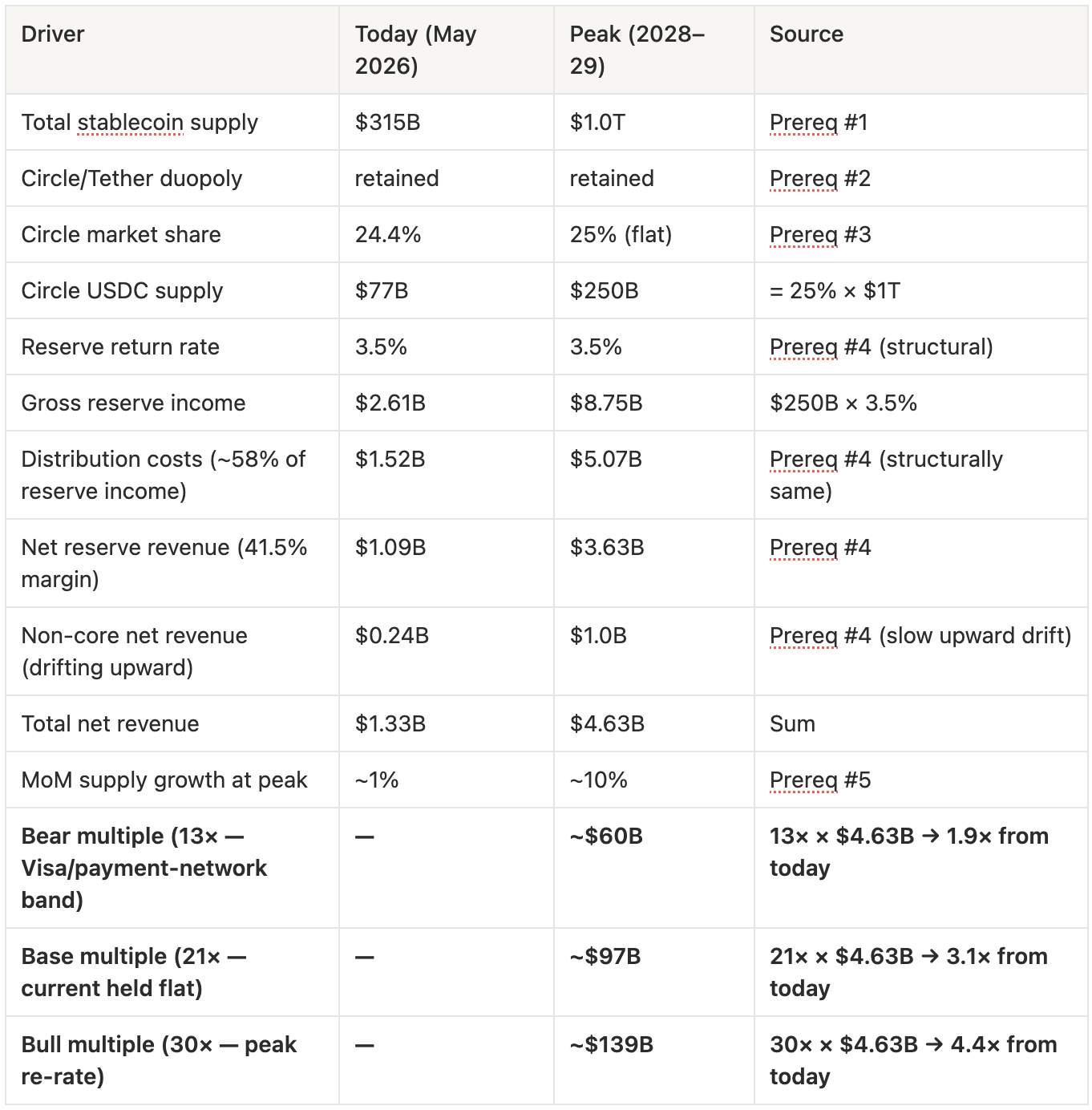

Tying it all together

Our Base Case is a combination of WAGMI plus nothing ever happens.

Stablecoin supply to grow to 1T next market cycle

Circle/Tether duopoly retained

Circle’s market share vs Tether is flat to rising — at ~25%

Net Revenue Margin is structurally the same, slowly drifting upward due to non USDC revenue

High marginal USDC supply growth ~10% MoM at the peak of the bull run

Same to higher net revenue multiples

Bear and Bull case mostly depends on Multiples as slight variation in resulting stablecoin supply

Our Trade - Coinbase Circle Barbell

Coinbase is capturing economics better than Circle. Circle is capturing market sentiment better than Coinbase. I plan to have more or less equally sized exposure to COIN and CRCL in the portfolio to position for this duality.

Both of the positions are core for our semi liquid Cycle Opportunities bucket allocations

~10% $CRCL

~10% $COIN

Saying that want to be cautious on the entry pricing. We’re not allocated yet anywhere but Bitcoin and assessing the market right now. It’s a relatively okay time to start DCA in, but not ready to get back for meaningful chunks yet.

Stay safe, grow and compound

One of the best takes on CRCL I've read in a while. I like how you frame it as a "network of acceptance", creating a duopoly, potentially similar to Visa/Mastercard or iPhone/Android. Will be interesting to see how the relationship between COIN and CRCL evolves.